Cyfrowy Polsat Group closed Q 3 2018 with very good operating results in both segments, and delivered strong financial results which reflect a healthy condition of the business. Furthermore, the Group exceeded 14 million contract services provided to its customers and thanks to the consistent multiplay strategy the churn rate was at the record low level. The Group has started monetizing the rights to the UEFA Champions League and generated very good sales results of the Polsat Sport Premium packages.

Major operating results for Q3 2018

- Bundled offers are used already by as many as 30% of customers – an effective execution of the multiplay strategy:

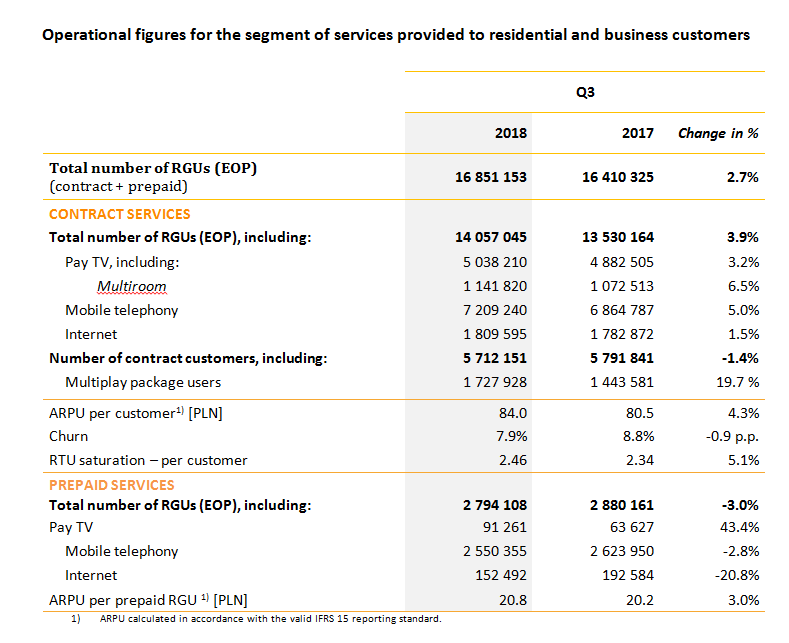

- Systematic growth of the multiplay service customers – up by 284 thousand (20%) YoY to 1.73 million (which constitutes 30% of the contract customer base).

- The number of services (RGU’s) used by this group of customers increased to 5.17 million.

- The above led to the reduction of the churn rate to the record low level of 7.9% per annum.

- Regular growth of the number of contract services – up by 527 thousand YoY– to 14.06 million (contract services account for 83.4% of all provided services):

- Another quarter with growth of the number of mobile voice services – up by 344 thousand YoY, reaching 7.2 million in total. This development is the outcome of the favorable influence of the adopted multiplay strategy, good reception of Plus’s new simple tariffs that were launched this February as well as high sales in the B2B segment (m2m solutions).

- Thanks to good sales of basic packages and value-added services (Multiroom and paid OTT services), the total number of contract pay TV services increased by 156 thousand YoY and exceeded 5 million.

- Internet access customer base increased by 27 thousand YoY and now stands at 1.8 million. During the first three quarters of this year, retail customers of Cyfrowy Polsat and Plus network transferred ca. 699 PB of data.

- Stable base of over 5.7 million contract customers:

- RGU saturation per customer increased by 5.1% YoY, with the average number of 2.46 services from the Group’s portfolio per customer.

- Average revenue per contract customer (ARPU), as calculated in accordance with the valid IFRS 15 accounting standard, increased by 4.3% YoY and reached PLN 84.

- Stable prepaid base of 2.8 million services reflects the actual user base of the prepaid service:

- High and stable ARPU from prepaid service, amounting PLN 20.8.

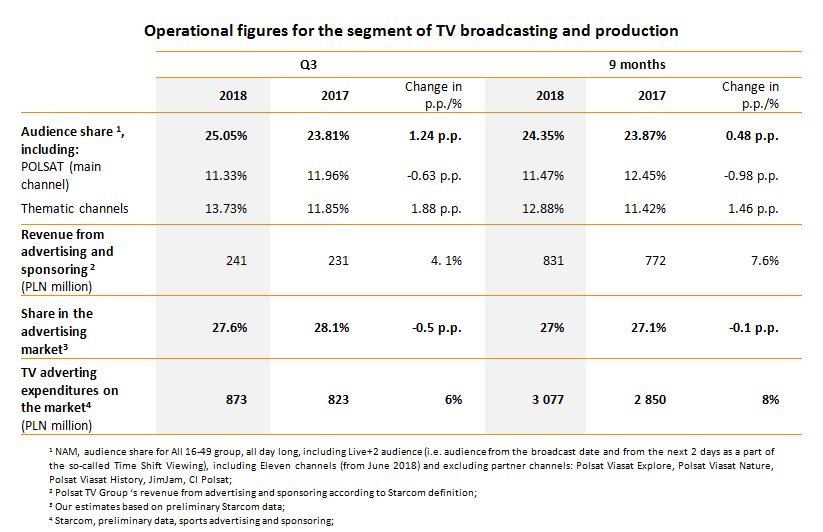

- In line with the long-term strategy, Polsat Group’s TV channels continued to stay at the top in terms of audience share in the commercial viewer group, both in Q3 and during the first 9 months of the year, achieving in the former of these periods the audience share of 25.1% (11.3% for the main channel and 13.7% for thematic channels) - in spite of a temporary adverse impact of the coverage of the 2018 FIFA World Cup in Russia which was broadcasted via free-to-air channels of the public broadcaster – and 24.4% for 3 quarters (11.5% for the main channel and 12.9% for thematic channels).

- Revenue generated by Polsat TV Group from commercials and sponsoring increased by 4.1% YoY in Q3 and reached PLN 241 million, thanks to which the Group’s share in TV advertising market reached 27.6%. During the period of 3 quarters revenue from TV advertising recorded growth by 7.6% and reached PLN 831 million, which have market share of ca. 27%.

“This was yet another quarter which gave us many reasons to be satisfied. A consistent pursuit of the development strategy in the area of multiplay offers brings very positive results. We already provide over 14 million contract services, 30% of the Group’s customers use bundled offers, and thanks to this we had a record low level of churn, which amounted to only 7.9% per year. Furthermore, we already see the first effects of strategic activities initiated after adding Netia to the Group’s portfolio” says Tobias Solorz, the CEO of Cyfrowy Polsat S.A. and Polkomtel Sp. z o.o. “We have started a multi-level monetization of the broadcasting rights to UEFA Champions League and Europa League matches, and the sale of the package including Polsat Sport Premium channels is at a very good level. Traditionally, we have prepared attractive offers for Christmas, which were made available to all our customers yesterday.”

“The audience results for Polsat Group channels in the commercial group in the third quarter and the first nine months of the year were in line with our long-term strategy, in spite of the strong impact on the market of the FIFA World Cup Russia 2018. A dynamic growth of our revenues from advertising and sponsoring, was supported by the fast implementation of the synergies announced at the moment of acquisition of new TV channels” says Maciej Stec, a Management Board Member of Cyfrowy Polsat S.A. and Telewizja Polsat Sp. z o.o. “Our investments into premium sport broadcast additionally strengthen the revenues of Polsat Group. We have enriched the portfolio of Polsat Group channels with new sport channels - Polsat Sport Premium and Eleven Sports, we have built the most advanced and modern sport studio in Poland dedicated to the UEFA Champions League and Europa League, we have prepared attractive offers with the above mentioned competition for the customers of Cyfrowy Polsat, Plus, IPLA and Netia and we were open to cooperation with other TV operators. The aim of all these activities was to ensure the best content in the best setting to all football fans.”

Major financial figures for Q3 2018

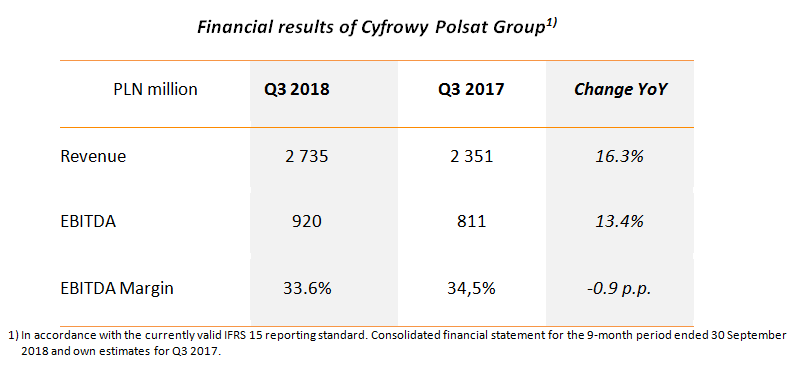

- The Group demonstrated strong financial performance (in accordance with the currently valid IFRS 15 reporting standard as well as while accounting for consolidation of Netia’s results; the historical data for 2017 is also presented in accordance with IFRSF 15):

- revenue: PLN 2.735bn (growth by 16.3% YoY),

- EBITDA: PLN 920m (growth by 13.4% YoY),

- EBITDA margin: 33.6%,

- Net profit: PLN 227.1m,

- Free cash flow for the 12-month period: 1.509bn,

- Total net debt /EBITDA LTM ratio: 2.83x.

- Growing financial results of the segment of services provided to residential and business customers (as calculated in accordance with the currently valid IFRS 15 reporting standard and while accounting for the consolidation of Netia’s results):

- Revenue: PLN 2.430bn,

- EBITDA: PLN 826m,

- EBITDA margin: 34%.

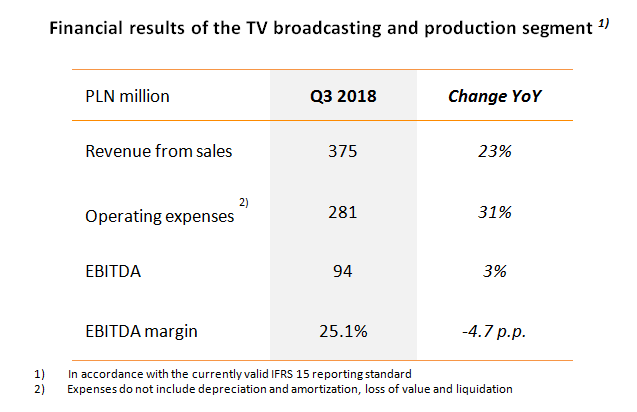

- Very good results of the TV broadcasting and production segment (as calculated in accordance with the currently valid IFRS 15 reporting standard):

- Revenue: PLN 375m,

- EBITDA: PLN 94m,

- EBITDA margin: 25,1%.

“The third quarter of this year is at the same time the first quarter of full consolidation of financial results of Netia and Eleven Sports Network. We have achieved strong financial results which reflect a healthy business condition of the Group and exceeds the average figures from analysts’ forecasts. This is due to very good sales results in both segments and consistent implementation of the multiplay strategy. At the same time, adding new TV channels, including premium sport channels, to the wholesale offer had a positive impact on the results of the TV broadcasting and production segment in this quarter. Free cash flows remaining at a high level offer comfort in the pursuit of our business strategy, investment plans and enable us to regularly repay our debt” says Katarzyna Ostap-Tomann, a Management Board Member responsible for finance at Cyfrowy Polsat S.A., Polkomtel Sp. z o.o., Telewizja Polsat Sp. z o.o.